A bonus from the government!

When you save into a pension, the Government rewards you with a ‘tax relief’ bonus, effectively thanking you for saving for the future.

This means that when you earn tax relief on your pension, some of the money you’d otherwise have paid in tax on your earnings goes straight into your pension pot.

Tax relief is paid on your pension contributions at your highest rate of income tax, i.e.:

Basic-rate taxpayers get 20% pension tax relief

Higher-rate taxpayers can claim 40% pension tax relief

Additional-rate taxpayers can claim 45% pension tax relief

And it’s something that’s back in the spotlight.

While it’s still around in its current form, then, just how good is Higher Rate Tax Relief?

Here's a simple calculation: let me introduce Bob.

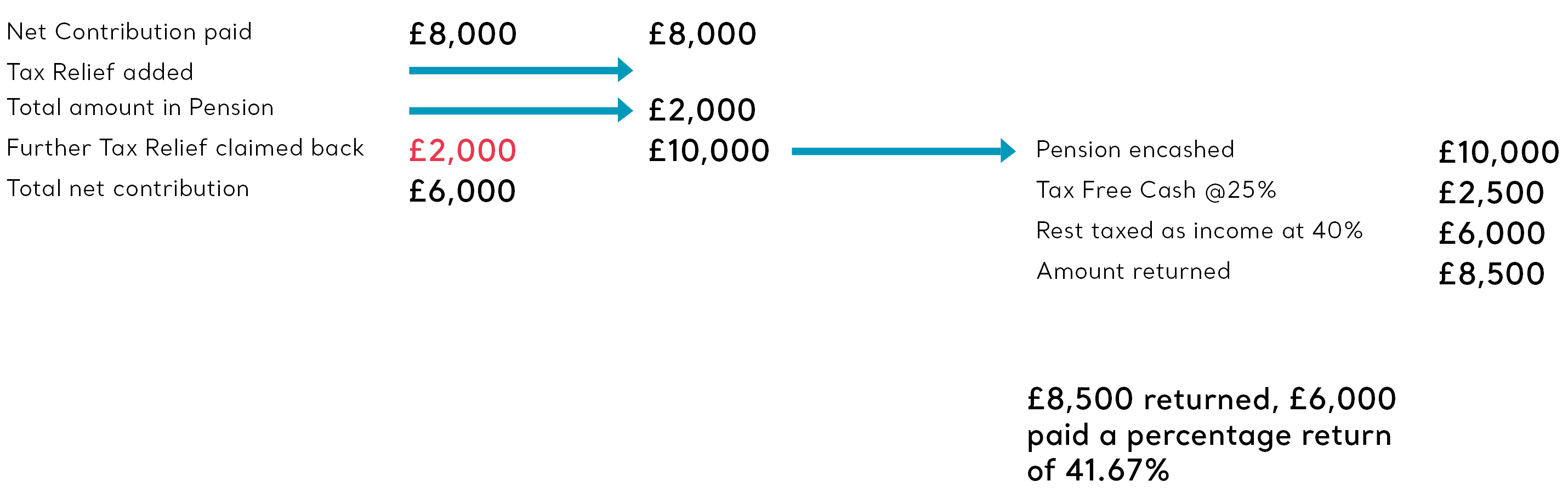

Bob, aged 55, pays a single contribution of £8,000 into his Personal Pension. This is then grossed up to £10,000 due to Basic Rate Tax Relief that is provided on Pension contributions.

However, Bob is a Higher Rate Tax Payer and so can also claim back a further £2,000 from HMRC, which he does. Bob then immediately asks how much of this he can take out should he wish to do so and he is offered this calculation.

He can have the first 25% as Tax Free Cash, which equates to £2,500. The remaining £7,500 is deemed as income and would be taxed at 40%, which leaves him with £4,500.

Therefore, if Bob removed all his money immediately, he would get £7,000 back (£4,500 + £2,500). You may recall that he paid in £8,000 BUT also got a further £2,000 back from HMRC.

This means that Bob’s pension contribution only cost him £6,000 and on day one it is worth £7,000 if he takes it all back. This is an increase of 16.67%.

But Bob has listened to his adviser at Punter Southall Aspire and he now knows that his best option is to wait until he is a Basic Rate Tax Payer, which should be the case once he retires. That would mean that he would have £2,500 Tax Free Cash but his remaining £7,500 would be worth £6,000 as he would only have Basic Rate Tax to pay.

That means he gets £8,500 back from a contribution that only cost him £6,000. That’s a whopping 41.67% return on his investment.

You can find lots more about pension planning here: The complete guide to a pension plan